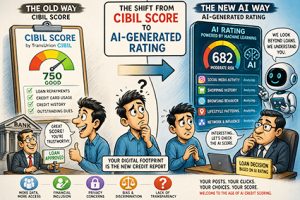

From Credit Scores to Digital Footprints: Will AI Redefine Personal Creditworthiness?

In India’s rapidly evolving financial ecosystem, the traditional credit score—long dominated by agencies like TransUnion CIBIL, Experian, and Equifax—may soon face disruption from a new, data-driven contender: AI-generated behavioral ratings.

From Credit Scores to Digital Footprints: Will AI Redefine Personal Creditworthiness?

For decades, an individual’s creditworthiness has been assessed using structured financial data—loan repayments, credit card usage, and borrowing history. But as digital footprints expand, lenders and fintech companies are exploring how artificial intelligence can analyze non-traditional data sources such as social media activity, online shopping habits, and browsing patterns to evaluate risk more dynamically.

The Rise of Alternative Credit Scoring

AI-powered credit scoring models rely on machine learning algorithms that process vast amounts of behavioral data. These systems can detect patterns that traditional scoring systems miss. For example:

- Consistent online purchases of essential goods may signal financial stability

- Social media networks could hint at professional credibility or lifestyle risk

- Browsing habits might reflect financial discipline or impulsive behavior

Fintech startups globally—and increasingly in India—are experimenting with such “alternative data” to assess individuals who lack formal credit histories, often referred to as the “thin-file” or “new-to-credit” population.

Financial Inclusion or Surveillance?

Proponents argue that AI-based scoring could significantly expand financial inclusion. Millions of Indians without formal banking histories could gain access to credit based on their digital behavior. For gig workers, freelancers, and young professionals, this could be transformative.

However, critics raise serious concerns:

- Privacy Risks: Continuous monitoring of personal data raises questions about consent and misuse

- Bias and Discrimination: Algorithms trained on biased data may reinforce social inequalities

- Lack of Transparency: Unlike traditional scores, AI models can be opaque, making it difficult for individuals to understand or challenge their ratings

Regulatory Tightrope

Regulators such as the Reserve Bank of India (RBI) are closely watching these developments. While innovation is encouraged, data protection and consumer rights remain paramount. India’s evolving data protection framework will play a crucial role in determining how far AI-based scoring can go.

Globally, regulators are already grappling with similar challenges. The European Union’s GDPR, for instance, includes provisions against fully automated decision-making without human oversight—a principle that could influence Indian policy.

The Road Ahead: Rather than outright replacing traditional credit scores, AI-generated ratings are more likely to complement them in the near future. Hybrid models—combining financial history with behavioral insights—could become the norm.

Banks and NBFCs may begin using AI scores as a secondary layer of assessment, especially for underserved segments. Over time, as trust and regulatory clarity improve, these models could gain mainstream acceptance. The shift from static credit scores to dynamic AI-driven ratings marks a fundamental change in how trust is measured in the financial world. While the promise of inclusivity and precision is compelling, it must be balanced against ethical considerations and robust oversight.

As India stands on the cusp of this transformation, the question is not just whether AI will redefine creditworthiness—but how responsibly it will do so.